Analyse May 2021

Is the sky the limit for property assets?

Video production: Le Temps

Property prices continue to rise, driven higher by the pandemic. Houses are expensive almost everywhere in Switzerland. You may be wondering if you can still buy without a second thought. That’s an easy question, and one that should be asked, but the answer is complex. At the moment, it is impossible to determine whether a property bubble may be forming.

No matter what you’re buying, a house, a commonhold property (PPE), a second home or an apartment building: everything is going up in price. This trend has been visible for several years. In the space of a decade, house prices have risen by 26% while commonhold prices are up 15%. Apartment buildings, which require huge cash piles (of the likes available to pension funds, for example), are no exception. These prices have also fuelled the uptrend, gaining by almost 10%.

There are countless houses throughout the country selling with a price tag of over one million francs. Of course, differences exist. For example, some houses still cost CHF 500,000 in La Chaux-de-Fonds or Visp. In contrast, even if you simply wanted an apartment, in Geneva, Lausanne, Vevey, Basel or Zurich, you’d have to spend at least a million, if not a million and a half francs. Nationwide, the median price is now CHF 1.15 million.

Some originally thought that the pandemic would slow the trend, effectively pouring cold water on the housing market. In fact, quite the opposite has happened. Forced to stay at home, Swiss residents are now thinking bigger, more modern, more comfortable or, why not head for the mountains? In 2020, prices advanced by a further 3-4%. Properties in the mountain valleys or in the Alpine foothills have gained substantially, having recovered from the effects of the Lex Weber. We have seen chalets and holiday apartments sell for up to 20% more than expected.

Spotlight on the housing market

This situation raises legitimate questions for investors. Chiefly, how long will the move last? Is it sensible to buy today without looking too closely at the price tag? When prices turn the corner, how precipitous will the fall be? Are we facing a speculative bubble much like the IT sector recently? All very complex.

For a better understanding of the market forces, let’s leave aside investment property and major investors and shine our spotlight on home buyers. Home prices are rising because people naturally want to own their own home. Compared with other countries, Switzerland is still a tenant’s market. But despite this, the size of the Swiss mortgage market last year exceeded CHF 1,000 billion – twice as much as 20 years ago. Housing demand is also supported by historically low interest rates. From close to 3% in 2010, the interest rate on a 10-year fixed-rate mortgage is now hovering around 1%.

When and how fast?

Will interest rates rise too quickly, as they did in the late 1980s, which resulted in a twofold increase in interest costs? The pundits have reassuring news. At that time, they point out, most mortgages were tied to floating rates. These days, the opposite is true. More than eight out of ten mortgages have been arranged at a fixed rate, meaning that their cost is locked in for a set amount of time. If interest rates do rise, borrowers will see their bills increase when they renegotiate their mortgages – not before. Rising interest costs will make new purchases more expensive, dampen demand and thus drive down prices.

The Swiss National Bank views the situation with circumspection. Its opinion is that the market has become more vulnerable. It is chiefly worried that some households might not be able to cover housing-related costs. Some property market researchers have drawn up red lists: Lausanne, Geneva, Zug, Zurich and their environs. Supply is desperately lacking in these regions, prices are too high and the market is too heavily dependent on low interest rates, which in turn increases the risk.

So how can we sum up the housing market at the moment? Perhaps like this: property professionals believe that the market is currently healthy, whether this be on the main plateau or in the mountain regions. Demand is persistently strong. There are no bubbles to report, so no cause for concern. So far the experts have been right. In any case, the economic literature on this subject is abundant, and its authors are overwhelmingly of the same view: a price move is only called a bubble once it has burst.

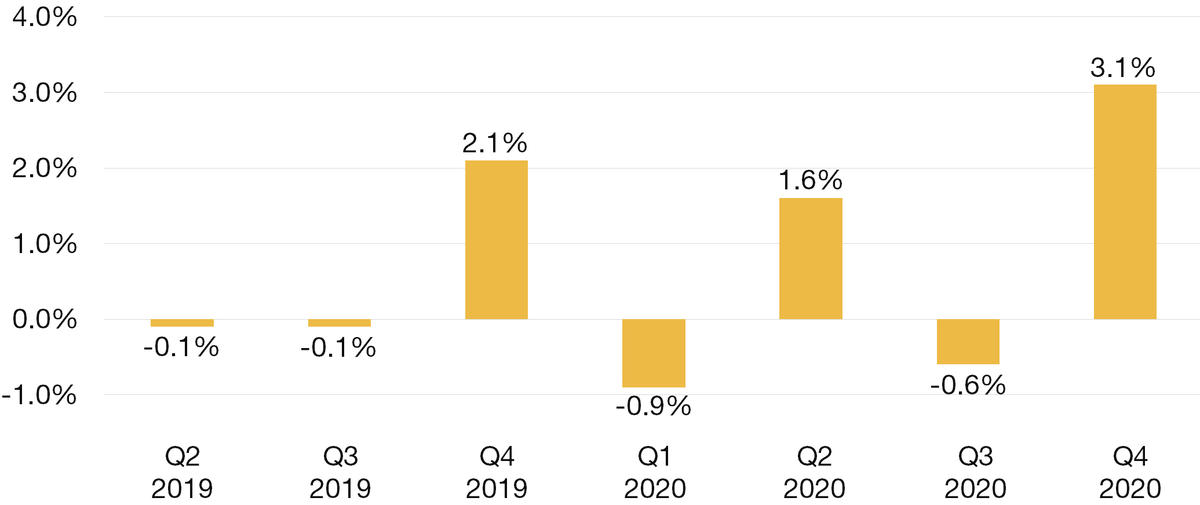

Fig. 1. Swiss House Price Index - Commonhold property (PPE)

Latest news from the Bonhôte Group

Bonhôte Impact Fund 12.5% return for investors, much more for humanity

Aiming to deliver a positive social and environmental impact, the Bonhôte Impact fund has gained by 12.5% since inception in 2019 amid extremely low or, in places, negative investment yields.

Bonhôte Impact’s managed accounts and the bespoke fund are renowned for combining strong returns and sustainability.

Appointments

The Board of Directors made the following appointments at its latest meeting.

Julien Stähli has been named Chief Investment Officer (CIO). He will continue to oversee discretionary investment management. Claude Suter has been appointed Head of UHNWIs & Independent Asset Managers. Cédric Huguenot, Head of Finance, now sits on the Executive Committee (ExCo).

Elodie Gilberti joins as portfolio manager

Elodie Gilberti, who holds a BSc from the Ecole Hôtelière de Lausanne and a CWMA (Certified Wealth Management Advisor) certificate from SAQ, has joined us as a portfolio manager based at our Neuchâtel headquarters.

She has extensive banking experience gained working for several renowned institutions.