27/03/2023

Flash boursier

Key data

| USD/CHF | EUR/CHF | SMI | EURO STOXX 50 | DAX 30 | CAC 40 | FTSE 100 | S&P 500 | NASDAQ | NIKKEI | MSCI Emerging Markets | |

| Latest | 0.93 | 0.99 | 10'613.55 | 4'064.99 | 14'768.20 | 6'925.40 | 7'335.40 | 3'916.64 | 11'630.51 | 27'333.79 | 951.56 |

| Trend | |||||||||||

| YTD | 0.21% | -0.18% | -1.08% | 7.15% | 6.07% | 6.98% | -1.56% | 2.01% | 11.12% | 4.75% | -0.50% |

(values from the Friday preceding publication)

Under the watchful eye of central banks

Equity markets pulled back from the brink last week, supported by decisive action from central banks that remain committed to taming inflation but are also ready to act if economic conditions should deteriorate.

As expected, the Fed raised its benchmark rate by 25bp to a range of 4.75-5.00%. However, the turmoil in the banking sector could force it to slow the pace of monetary tightening if necessary.

In the US, the robust labour market continues to support economic activity, with initial jobless claims dipping by 1,000 over the past week to 191,000.

Growth in US private sector activity accelerated markedly in March, with the composite PMI rising to 53.3 from 50.1 in the previous month. The preliminary services PMI rose sharply to 53.8 in March from 50.6 in February.

The US Commerce Department reported that US durable goods orders fell 1% last month, following a 5% drop in January. But excluding transportation machines, these orders were more or less stable.

Meanwhile the Swiss National Bank (SNB) raised its benchmark rate by 50bp to 1.5%, taking a confident stance in the wake of the support measures for Credit Suisse, which is being taken over by UBS as part of an emergency rescue plan. The SNB also indicated that further rate hikes were not out of the question in order to curb inflation.

The Bank of England (BoE) also announced a 25bp hike in its key interest rates after consumer price inflation (CPI) unexpectedly accelerated to 10.4% year-on-year in February. Economists had expected a slowdown to 9.9% after a reading of +10.1% in the previous month. Excluding energy prices and other volatile items, prices rose by a stronger-than-expected 6.2%, following a 5.8% increase in January.

Against this backdrop, the S&P 500 ended the week up 1.39%, while the tech-heavy Nasdaq rose 1.66%. The Stoxx 600 Europe rebounded by 0.87%.

This week will be overshadowed by the release of preliminary German and Eurozone inflation figures for March and US PCE inflation.

Banks under pressure

Policymakers tried all last week to reassure the public about the health of the financial sector.

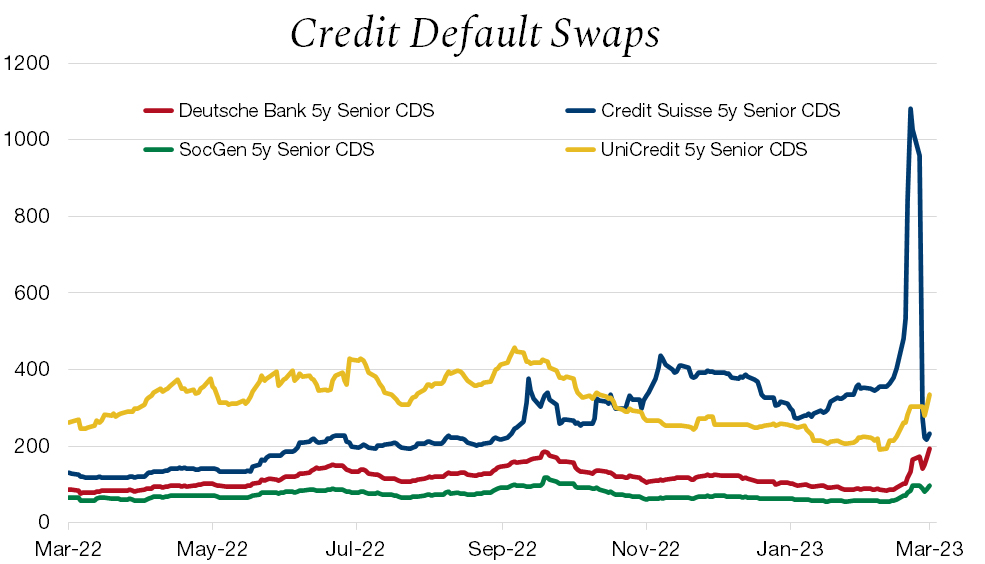

However, the collapse of three US banks and the Credit Suisse affair have caused cracks to appear in financial markets in response to the hawkish tightening of key interest rates. Although systemic risk is low, the impact of rising interest rates may not yet be fully reflected in the credit spreads of banks and other companies. This was partly demonstrated on Friday when we saw a rise in the price of credit default swaps (CDS) on several large European banks. As the chart shows, although CDS prices have risen, they are nowhere near the peak seen in the final days of Credit Suisse.

The banking sector is under pressure, with share prices plummeting and wiping out the gains made so far this year. This is despite the intervention of regulators who are committed to the soundness of the system. However, the risk of contagion is low, existing regulations in Europe are sound and banks are better capitalised (and therefore more resilient) than they were in 2008.